Why Businesses using Blockchain Technology are Filing for patents and Other Useful Info about Software Patents

“Open” Source: Can you Patent the Blockchain?

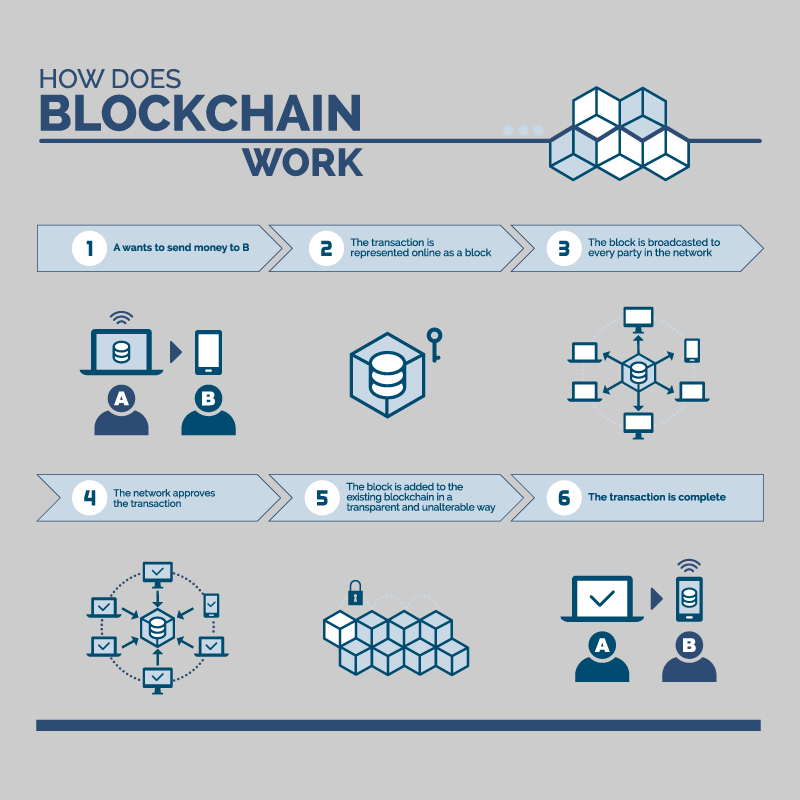

The Blockchain is now firmly in the public eye, placing it at a crossroads. This technology that fuels Bitcoin and many other virtual financial applications, coins, and software, is a revolutionary force in financial transactions. But it was originally invented to be open source shared by all. And now more and more companies are taking that open source and using it for their things, pushing this shared resource into a protracted legal debate involving patent law. You don’t have to be a law school student or have passed the state bar to know that the Blockchain could be headed toward a patent war.

Can you patent the Blockchain?

Some firms, like R3, say they would make their Blockchain software open to the public, keeping in harmony with the pseudonymous inventor Satoshi Nakamoto’s vision. But other companies, such as Goldman Sachs, seek a patent for “processing financial transactions using a distributed ledger to store a portion of the ledger corresponding to a respective asset” which in layman’s terms is exactly what the Blockchain does.

While Goldman Sachs got the lion’s share of the media spotlight, and the ensuing backlash, there are hundreds of companies seeking patents from the patent office involving the Blockchain, including giants such as Bank of America, Accenture, and Morgan Stanley. And Craig Wright is making claims to have invented bitcoin, filing dozens of patents in an attempt to also control the intellectual property rights of the Blockchain open source code.

How open is the open source at this point?

Well so far, the United States Patent and Trademark Office (USPTO) has yet to grant any of these patent applications. If the USPTO does grant a patent, however, patent agents and IP law firms are going to be very busy because blockchain has already revolutionized financial transactions throughout the world.

It’s inevitable that a patent war will happen. And either thousands of injunctions could occur, or a “patent trolling” tactic where the patent holder creates shell companies to file lawsuits for violating a patent, takes place. Millions upon millions of dollars are at stake.

Don Tapscott, a co-author of a popular book, Blockchain Revolution, a surge of patent litigation could be devastating to the technology’s development, told Fortune Magazine: “This sort of behavior is antithetical to innovation, collaboration and the openness that’s at the heart of the new digital age,” said Tapscott. “I find it unfortunate when incumbents threatened by new paradigms revert to behavior that’s not even in their interest.”

Why wasn’t the Blockchain patented when it was invented? It was created by Satoshi Nakamoto (pseudonym). He published a white paper on Blockchain and coded the first implementation. Since then, no one has heard from him. The core of Blockchain’s technology is public domain thanks to the release of that paper. Only additions and variations of the core tech can be patented. For example, Chinese telecom giant Huawei seeks to patent Blockchain rights management. Huawei claims to have an invention that adds a verification feature to a content distribution network powered by Blockchain.

Protect Technology with a Patent

So, why are patents even necessary? One word: protection. The patent process provides the patent practitioner key protections from patent infringement under the law. This is what Goldman Sachs suggests is their motive for the Blockchain patent filing. The best way to acquire protection is to hire a professional patent attorney and file for a patent.

A patent is a set of rights granted to a person or company that created an invention or idea which protects it from competitors who would try to make it, sell it, use it or offer it for sale. In the U.S., the term for a patent is 20 years from the date on which the patent application was filed; often with an IP lawyer. And it takes a while to get a patent. The application must be filed within one year of public use or publication.

Also, the patent application process lasts 3 to 5 years and are very expensive in legal and consulting fees, but having a Philadelphia patent lawyer could alleviate any confusions.

When it comes to the blockchain, filing for a patent is tricky since only parts of it can be patented. Blockchains have different forms, and some of the blockchain technologies have patent protection. Thus, those who are scrambling to patent blockchain technologies are from the information technology and financial industries. It’s interesting to note that no single company owns all the blockchain-related patents.

As Paul & Paul have noted in the past, patent applications involving forms of software, like the blockchain, face an extremely high bar due to the Supreme Court ruling in the case called Alice. That SCOTUS decision ruled most software patents are abstract ideas that are ineligible for patent protection.

Any such patent applications, even provisional patent applications, would also have to overcome objections that the “invention” in the claim is obvious. This is especially the case because the applications are not for foundational concepts like bitcoin or the blockchain itself. Both Bitcoin and the Blockchain are concepts that could not be patented today since bitcoin’s creator, Satoshi Nakamoto, released them to the public years ago. If Satoshi Nakamoto had gotten a patent for blockchain, none of the patent frenzies would be happening.

On the face of it, the blockchain does not lend itself to making strong intellectual-property claims. Satoshi Nakamoto published a paper about his invention, coded the first implementation and then disappeared from the public eye. This strongly suggests the core of the technology is now part of the public domain. That means only important additions and variations to the core technology could be patented, not the technology itself. And the blockchain’s components are widely known. In the United States, court decisions, as well as a new law on the granting of patents, make it difficult to claim ownership for such financial innovations.

Corporate Use of the Blockchain

The open-source sharing of the Blockchain by Satoshi hasn’t stopped firms from trying to get patent protection on meaningful improvements to the blockchain, including security and encryption techniques, Colette Reiner Mayer of Morrison & Foerster, a law firm, told The Economist.

Heated fights over intellectual property are nothing new in emerging technology markets. But given that the blockchain is expected to shake up everything from the way precious diamonds are safeguarded to the way shares are traded, the legal fights could be especially fierce. A large number of companies plan to use blockchain technology:

- Coinbase

- Microsoft

- Bank of America

- MasterCard

- Amazon

- Apple

All of these companies have filed for blockchain-related patents. Many companies are rushing in to get provisional patents before the technology is even on the market. In addition to providing protection, patents make companies more attractive to investors because it shows they have something very valuable and worth protecting.

They will also benefit from cross-licensing. This means that one company can grant another company the rights to a piece of the product, research or subject. From a legal standpoint, cross-licensing is another form of protection because both companies can avoid infringement disputes and litigation. The companies that use blockchain can be part of a patent pool, which protects members against lawsuits. Some may even sign a patent pledge, a document that states an organization will not sue other companies.

Only a very few patents have been issued so far. And known applicants all say that they intend to use patents only “defensively,” meaning to protect themselves against lawsuits.

To limit such fights, several startups are opening up their Intellectual property. Among them, Chain, Digital Asset Holdings, and Hyperledger have made their software open-source, so that the underlying architecture is freely available to both users and developers. Some programs even come with a license that makes it impossible to enforce patents against those who use the organization’s code. Blockstream, another startup, has signed a “patent pledge,” vowing not to sue others—as long as they don’t use their patents offensively.

There are also discussions over forming a patent pool, much like the Open Invention Network, created in 2005 to protect member firms against suits for using Linux, the popular open-source operating system. The OIN acquires patents and then licenses them freely to members, which agree not to assert their patents.

Whether this strategy of mutual disarmament is sufficient to avoid another patent war will be clear only when and if blockchains have become a multi-billion dollar business.

Philadelphia IP Lawyers

In the tri-state area, no one knows patent law than patent practice law firm Paul & Paul. With new technologies and inventions being created every year, the need for patents has never been greater. Our intellectual property rights attorneys know what’s at stake if you don’t protect your invention or idea. All that hard work is gone – used by someone else and claiming it as his or her own. We also handle other legal services including matters concerning trademarks, copyrights, and trade secrets both domestic and foreign.

For 170 years and 40 countries, innovators and entrepreneurs have trusted our legal team to guide them with expert legal advice on intellectual property law. Whether you are a small business owner or a large corporation, contact registered patent attorneys Paul & Paul today for free consultation. We will take the time to sit down with you to go over a strategic plan to safeguard your idea or product. You’ll learn if you need to get a patent, how to file a patent application, how your intellectual rights will be maintained in another country and more.